Going (Almost) All Cash

Your permission slip to listen to Mr. Benner

Several months ago I went on a family trip to Lake Norman in North Carolina. It’s probably better to say I took my family on a trip, because any dads out there know that it’s not really a vacation when you’re playing tour guide, crisis negotiator, and money machine for the kids and everyone under your wings.

But really, it was a great trip. We got to swim in the lake, pet some wild deer, and I even burned a hole in my shoe during the evening campfire sessions. My kids got a kick out of that, after I had been warning them not to swing around coal-studded fire pokers.

While we were there I had a friend stop by for lunch who manages a large family office hedge fund based in Charlotte. He’s been successfully managing the fund for almost 20 years and I try to lap up any wise words he shares with me.

Looking out over the lake, out conversation quickly turned to the markets. Silver and platinum had just begin to make their meteoric rise, catching up to gold’s historic run after years of dormancy.

Having a lot of exposure to those metals and miners in my fund I mentioned that I was considering going to cash. My rationale was that I was uncomfortable with the enormous gains I was seeing in such a short amount of time. Of course the gains were great, but what was coming next?

I wasn’t seriously going to go into cash, but the comment I made sparked a broader conversation.

“You know,” Cody, my mentor said, “That’s one of the biggest challenges with investing and managing money for the long term. There’s always a temptation to bank your gains, but sometimes you just end up killing your momentum.

“But the bigger issue is not with killing your momentum,” he continued, “It’s that you always need to have your next move planned before you feel the urge to sell anything. Managing money is just as much about building a long term path as it is about the real time management part. That’s why very few people can do it long term. It’s difficult, exhausting, and sometimes feels impossible.”

Our conversation wondered off in some other direction, but his words have stuck with me - and they are especially relevant today.

Over the past couple of weeks I have been selling off much of my fund, taking profits in anticipation of new deep value plays ahead. This has been a difficult process, especially when I think about that conversation at Lake Norman.

But the data and information I’m looking at are telling me to take caution right now… And that was before the conflict in the Middle East broke out.

Mainstream’s Narratives

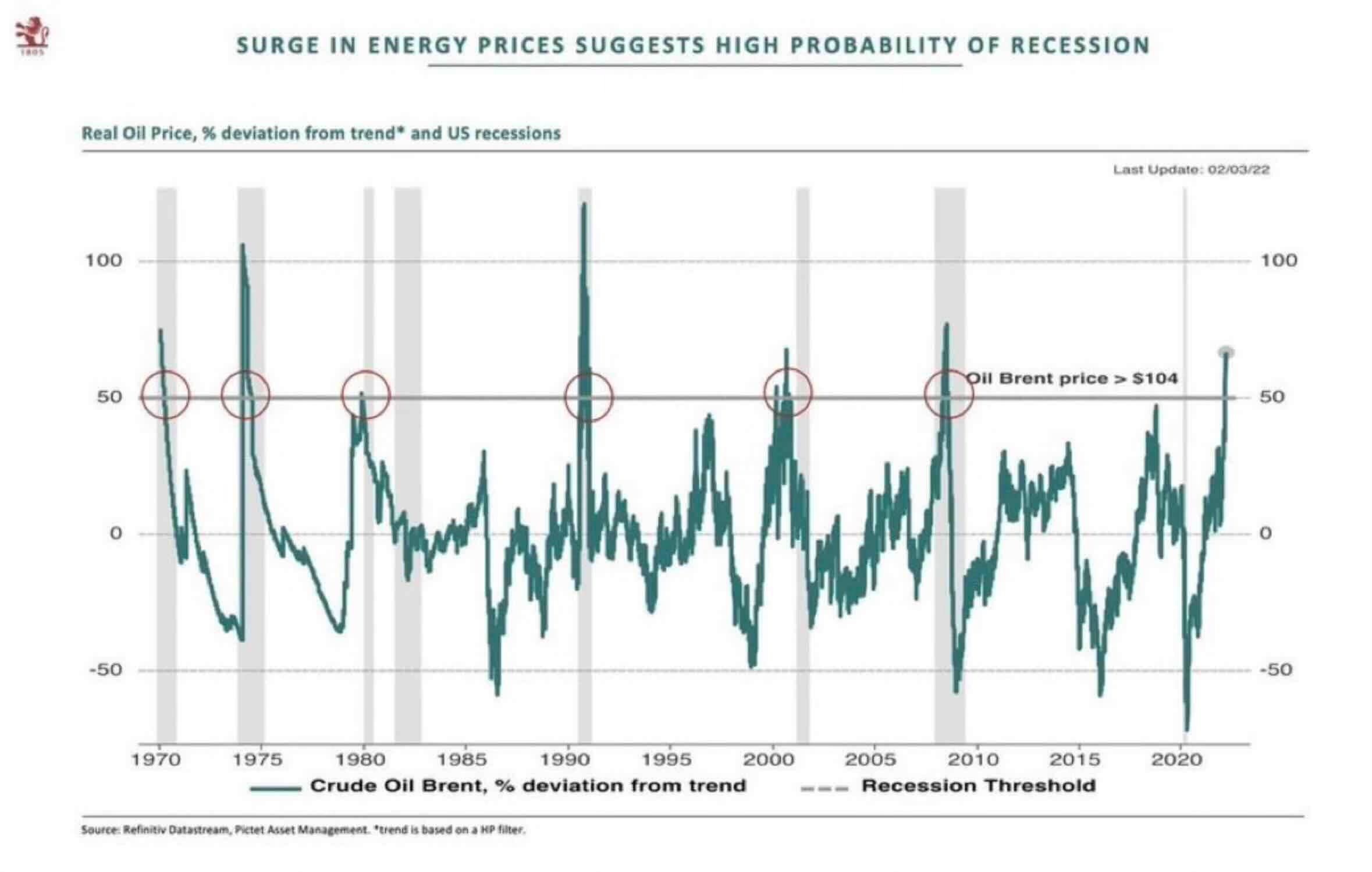

Let’s take a quick look at the obvious first: oil and gas.

The correlations of oil spikes and economic recessions are stunning. The only time an oil spike didn’t result in a recession was most recently in 2022. But, as I’ve explained in depth before, that time didn’t count. (Really, it didn’t!)

Source: Thierry from arvy

I have been looking at similar charts for the past year, which is one of the lessor reasons why I’ve been overweight in oil and gas over the past six months. The main reason was because oil and gas equities were trading at historically low valuations relative to… Everything!

My thought, other than the obvious value part, was that I’d like to be positioned in something that will rally and sing like a canary when trouble is coming. I think we’re there, or at least very close.

What’s interesting with this current oil rally is that it coincides with equity markets that are near all time high valuations. In fact, this past January marked the highest market cap to US GDP ratio in history (Warren Buffett’s favorite metric), at 220%.

Without taking into account a broader historical context, one would think that the current oil spike is purely attributed to the war in Iran. Zooming out, this oil spike would seem unordinary, assuming that all market run-ups proceeding recessions include a last hurrah from dinosaur bones.

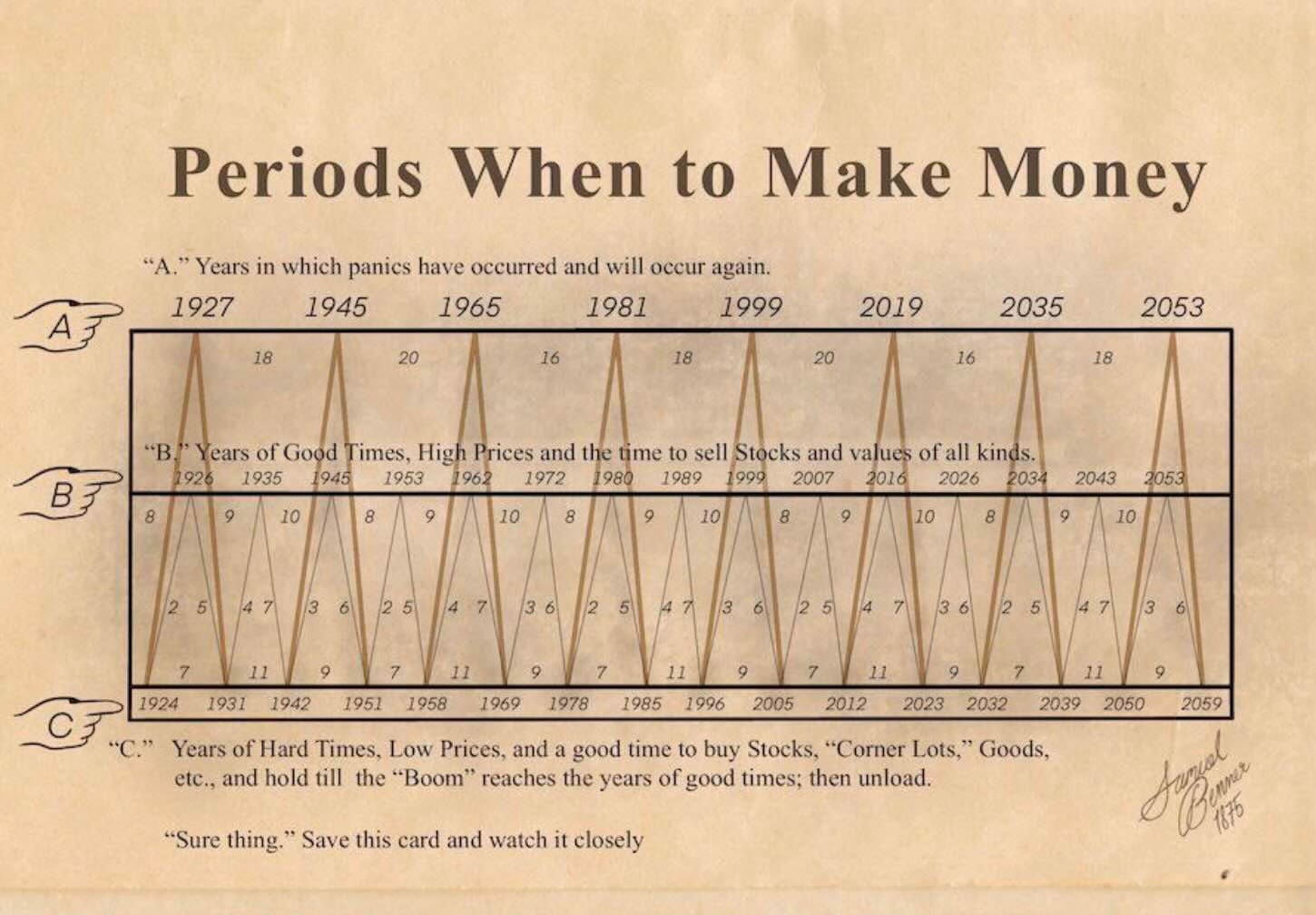

Maybe that’s the point: We’re losing sight of the broader cycle and blaming price fluctuations on conveniently timed geopolitical crises. Maybe this is all just the broader master plan, which has been foretold by Mr. Benner:

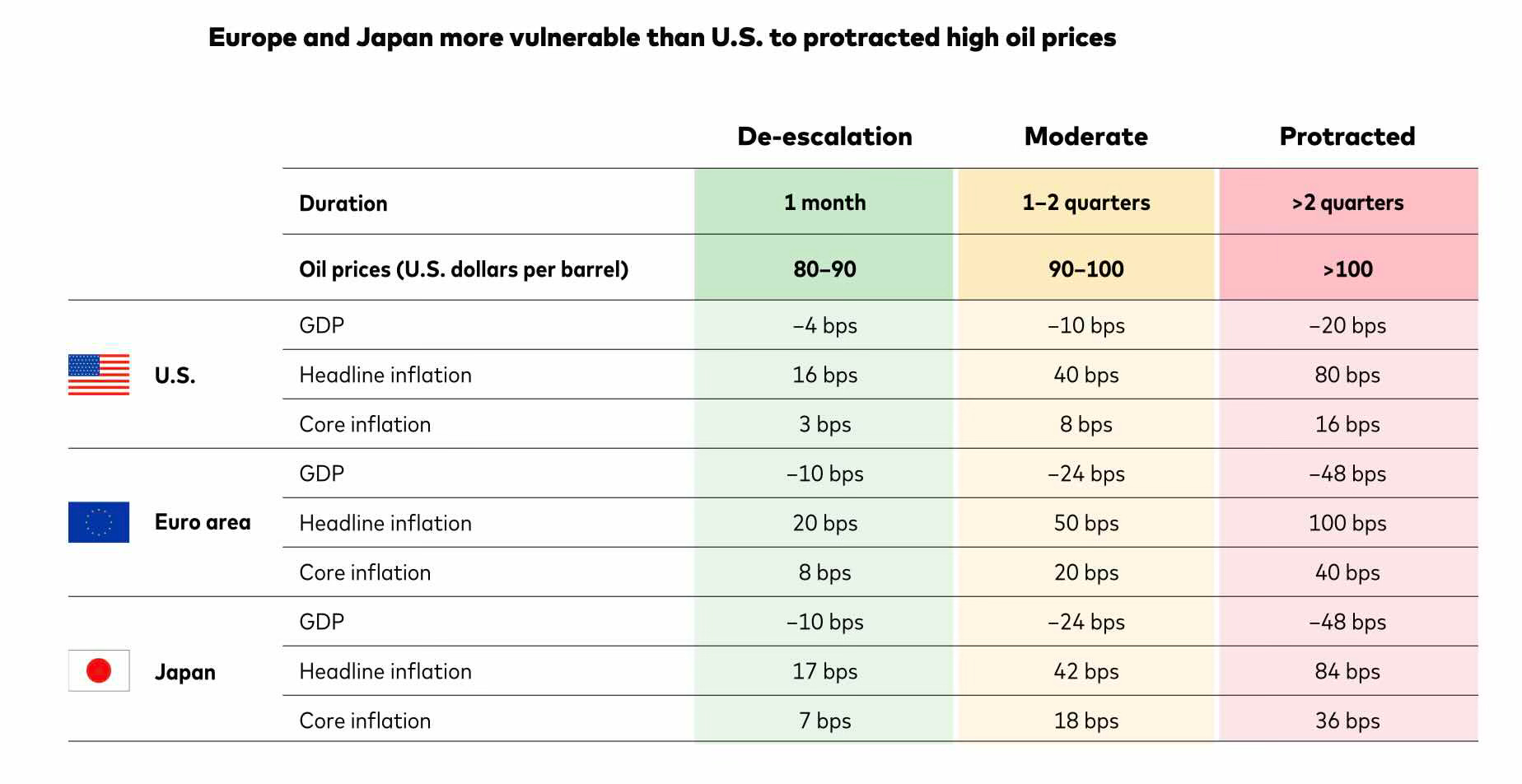

Continuing on the current oil theme for a moment, the main concerns for market participants relate to how long we’ll have an oil crisis. How long will the Strait be closed?

The data is clear: The longer oil prices stay high, the more devastating the results.

Source: Vanguard

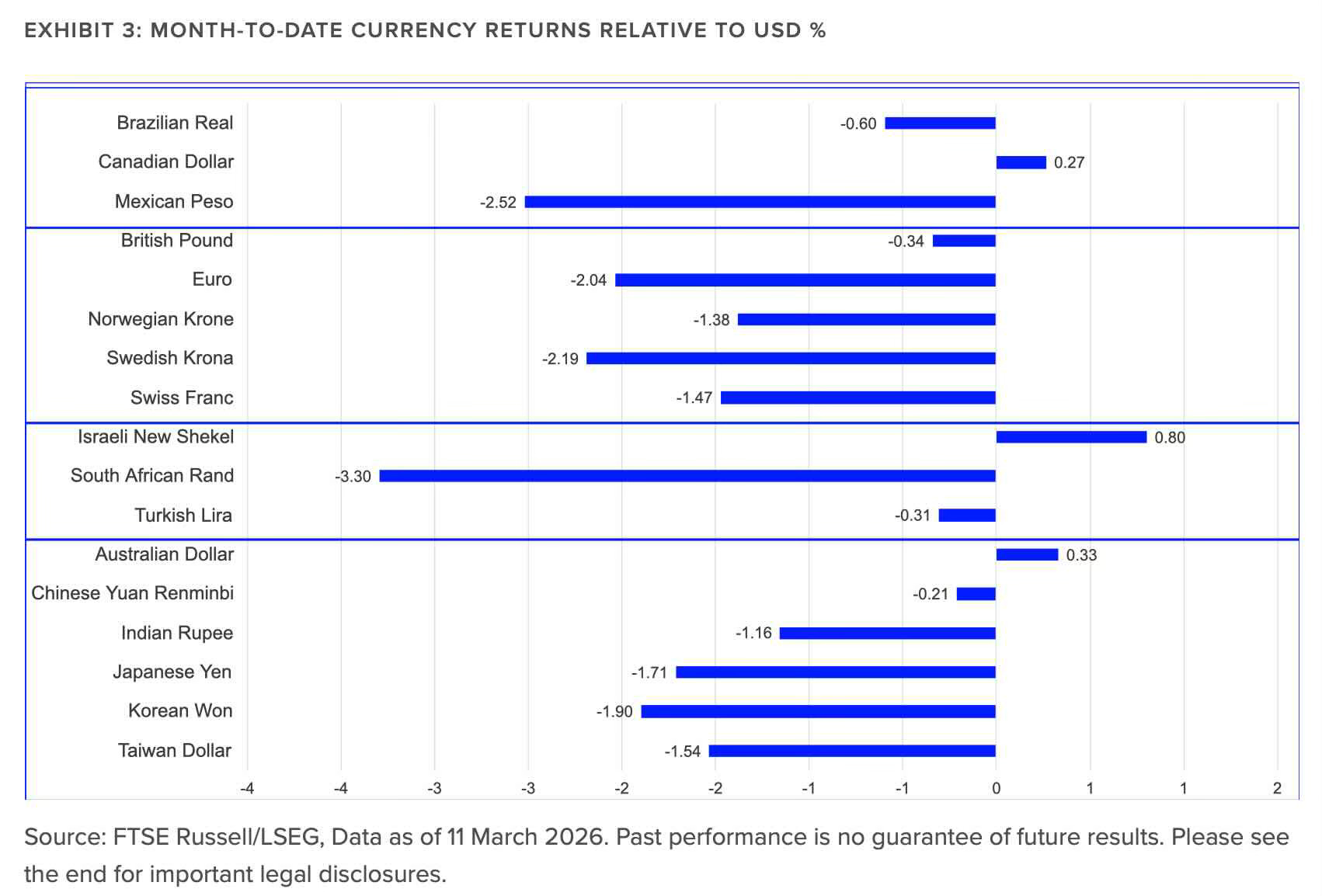

This is especially true for countries outside of the US, and their currencies.

Source: LSEG

This will weigh heavily on investors who have recently been rotating out of expensive US markets and into other parts of the world. As Reuters stated last month:

U.S. investors are pulling money out of their own stock market at the fastest pace in at least 16 years as Big Tech returns fade and better-performing overseas markets look more attractive.

In the last six months, U.S.-domiciled investors have pulled some $75 billion from U.S. equity products, with $52 billion flowing out since the start of 2026 alone, the most in the first eight weeks of the year since at least 2010, according to LSEG/Lipper data.

For the beginning of 2026, it was a great move - emerging markets and certain key US partners have had explosive returns lately. South Korea’s KOSPI saw a nearly 40% gain in the first two months of the year alone.

But, have investors jumped the gun by venturing outside the US too soon? The dollar index has sharply reversed trend as oil has ripped, and increasing energy costs tend to drag down non-US economies dramatically more.

Investors know this and have already been selling off many foreign tech companies in preparation for international consumer weakness. Alibaba ( BABA 0.00%↑ ), Sea Limited ( SE 0.00%↑ ) , Nu Holdings ( NU 0.00%↑ ), MercadoLibre ( MELI 0.00%↑ ), and many more have sold off aggressively since the start of 2026.

These company’s valuations, which are actually very attractive right now, may rise dramatically in the near future if weak consumer spending pulls down revenue generation. This, in turn, will drive those equity prices even lower as investors search for opportunities at fair value and steady growth.

The general consensus right now is that this scenario will happen due to our global oil shock that will lopsidedly effect those company’s target markets… Unless we have a very sharp reversal of what is going on in and around Iran.

What Mainstream is Missing, or at Least Ignoring

Beyond the current oil shock and geopolitical developments - which are still unfolding - there are a variety of data points that have piqued my interest over the past couple of years that relate to certainty.

Specifically that we, as investors and as a society, have an ever declining amount of certainty with nearly everything.

Some of this uncertainty is part of a normal cyclical process, like the election cycle. 2026 is a mid-term election year in the US which naturally brings up a lot of questions for where the country, and as a result much of the world, is headed.

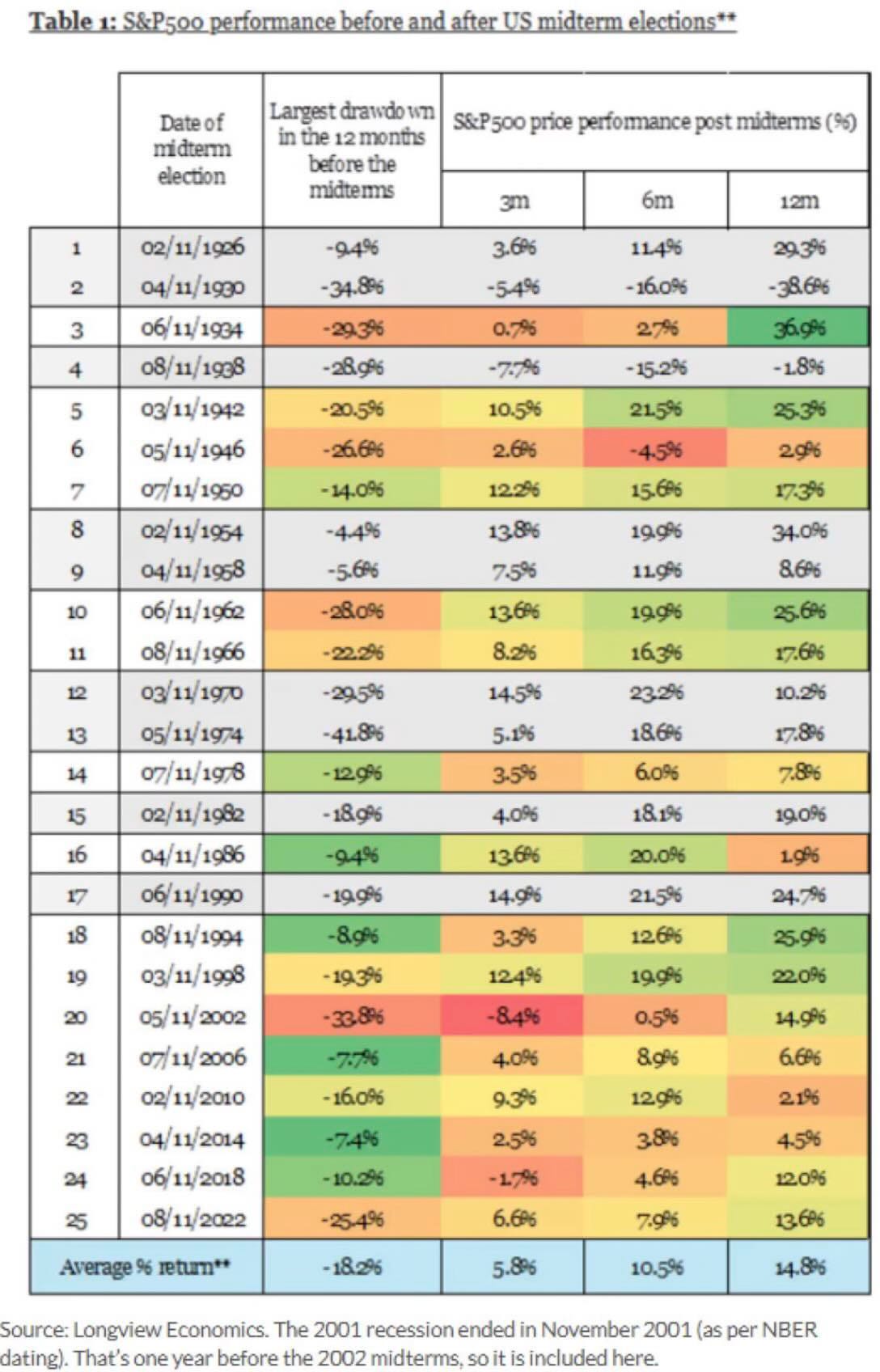

Source: Longview Economics

Market drawdowns during mid-term election years are, simply put, not good. And it makes perfect sense why. Whether it’s new policy that will overturn certain market trends or individual elected officials that could alter global initiatives, the 12 months proceeding the mid-term elections have historically been very volatile.

Since November 3, 2025 - which is the beginning of the 12 months proceeding the 2026 US mid-term elections - the largest (peak-to-trough) drawdown in the S&P 500 has been -7.55%. This is well below the average of -18.2%, and would make it one of the lowest drawdown years ever.

Of course, we still have eight more months until the mid-terms… There’s plenty more time for things to happen!

Once in a Lifetime Uncertainty

The mid-term election uncertainty is just a blip on the radar. It really doesn’t matter in the grand scheme of things, especially since we know it’ll happen again, and again, and again.

There’s another, much more important, cyclical uncertainty event that we’re all currently living through. The problem with this one is that it only comes around once in every generation. So, despite it’s cyclical nature, it’s really a one time experience for all involved.

That’s AI.

A quick disclaimer: I am not an AI zealot, nor have I been meaningfully invested in any specific AI company. But I do recognize it’s immediate and potential impact on society.

Not since World War II, has the world lived with the type of uncertainty it has today. I’m cautious to co-mingle historically significant events that included enormous amounts of tragedy and death, but the net result of the scenarios of today and of the past are likely to be very similar: We’ll soon be in a world that is nothing like today, and is currently nearly impossible to forecast accurately.

Of great importance is that no one has lived through an event like we’re currently experiencing. One where the future looks so uncertain that any significant investment of time, money, or energy may be a complete waste.

Again, this is not saying a period of extreme uncertainty hasn’t happened in the past. It just hasn’t happened during our personal lifetimes, which positions us individually in a very unfamiliar situation.

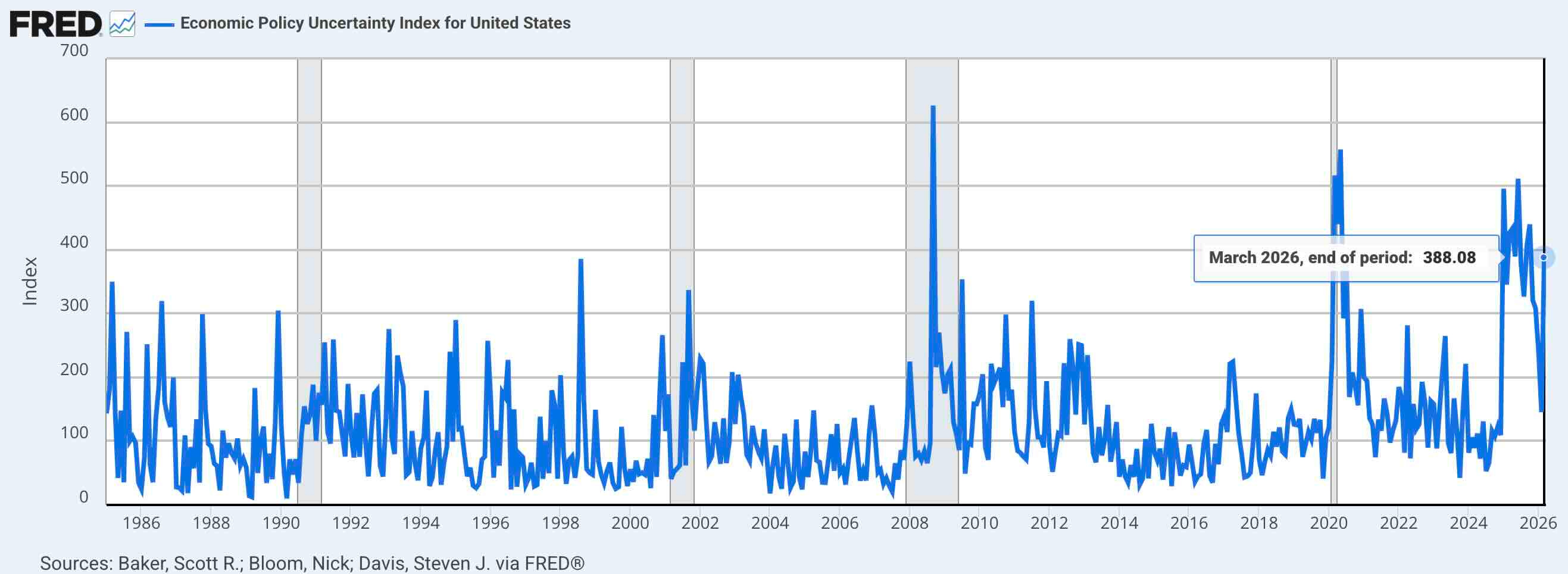

To be sure that my ‘extreme uncertainty’ remarks are not hyperbole, take a look at the Economic Policy Uncertainty Index for the United States:

Source: FRED

The elevation of the index ‘uncertainty level’ is just as important as the time this level is sustained at that elevation. As you can see, there is no other time in the past 40 years that even comes close. While data doesn’t exist (or at least I can’t find any) for the time period during WWII, I’m sure a similar index would look the same or even much worse. Regardless, none of us have lived through two of these events, making our current ‘certainty feelings’ incomparable.

Musical Chairs - You Don’t Have to Play

Investing is often a game of musical chairs. When one opportunity disappears, you have to find a new one quickly to keep your capital hard at work. Not deploying your capital - as in, not finding a chair to sit in - means you’re out of the game.

By the logic of many investors, including my mentor, you always need to be in the game. Even long term data shows that staying in the market always pays off.

As Buffett says, “Time in the market beats timing the market.”

But we also know that Berkshire holds the highest percentage of cash, ever, at over 30%, which is nearly $400 billion.

Do as he says? Or do as he does?

Your Permission Slip

Maybe you’ve read this far and thought to yourself, “Was this just some kind of cognitive dissonance exercise so Cody could justify his increased cash position within his fund?”

Perhaps there’s a bit of truth to that. Has there been anything written in world history where an author argues that their point of view is wrong?

Beyond my selfish current perspective, I truly do believe that most market participants have been conditioned to favor risk over caution for far too long. The FOMO, buy-the-dip, fintwit-compare-your-dick-annual-returns have all gone on long enough to seem completely normal.

It’s not.

So here’s your permission to take some caution.

There will always be new opportunities around each corner… But you can’t take action if you haven’t positioned yourself to exploit those opportunities.

That’s a fair way to think about it.

But concentration cuts both ways—conviction can amplify returns, or it can amplify mistakes.

The real question isn’t whether the opportunity set is uneven.

It’s whether the process for identifying “best ideas” actually holds up when the cycle turns.

Conviction matters. So does being wrong at size.

In converting to cash, you are describing "optionality." The editorial bias of self-directed financial newsletters is "take action," usually on the long side. Sitting on your hands, conserving cash, is boring; it also requires patience and discipline in an environment where AI, Tesla, Palantir, et al are "redefining the world." Everyone wants to be on the front end of the "next big thing."