Following the Capex Cycle

It's so simple that it might be stupid.

One of the biggest lessons I’ve learned over the many years of investing is to avoid the temptation to over complicate things.

This is especially true when someone is trying to justify an investment thesis they currently believe in, or are trying to sell.

The backflips someone will go through to explain why they are correct is often times laughable (I’ve been guilty of this plenty of times).

That’s one of the reasons why novice and expert investors have long respected the quotable wisdom that has come from Buffet and Munger.

Their overall investing strategy is quite simple: buy value based companies that you can understand for the long term and stay patient.

Warren’s most recent explanation for why Berkshire is holding so much cash is equally as simple: despite the recent market pull back, things are still expensive.

This sentiment, at least for the past year, has been in direct opposition with the general market who have been entrenched in the ‘AI trade.’

It’s hard to deny the recent success of this positioning. Artificial Intelligence really is starting to disrupt many parts of our daily lives. It’s very easy to imagine how these disruptions will eventually engulf the entire world.

But recent geopolitical and market developments are pushing back on this AI narrative.

The question, at least for the short term, is which will prevail?: The virtual world, or the physical world?

And equally as important: How many complications do we need to consider to forecast what comes next?

Virtual vs. Reality

For the sake of what I’m about to lay out, let’s make two assumptions:

Virtual = the impacts of technology, like AI, to all things that we can’t physically touch or extract from the earth.

Reality = all of the everyday things that our bodies physically come into contact with, including the materials that are pulled out of the earth to build our societies.

I don’t think anyone would disagree about the success the virtual world has seen over the past several decades. A mind-boggling amount of value has been built in the virtual world which has created enormous benefits for humanity, and investors.

But the success of the virtual world has mostly come at a huge expense for the real world.

Energy, agriculture, mining, manufacturing, and all kinds of physical world sectors have been ignored and starved of capital over the past decade.

Their capex cycle of the 1900’s has appeared to pause… for now.

Chart taken from a recent article:

The disconnect could snap back violently.

Tech vs. Energy

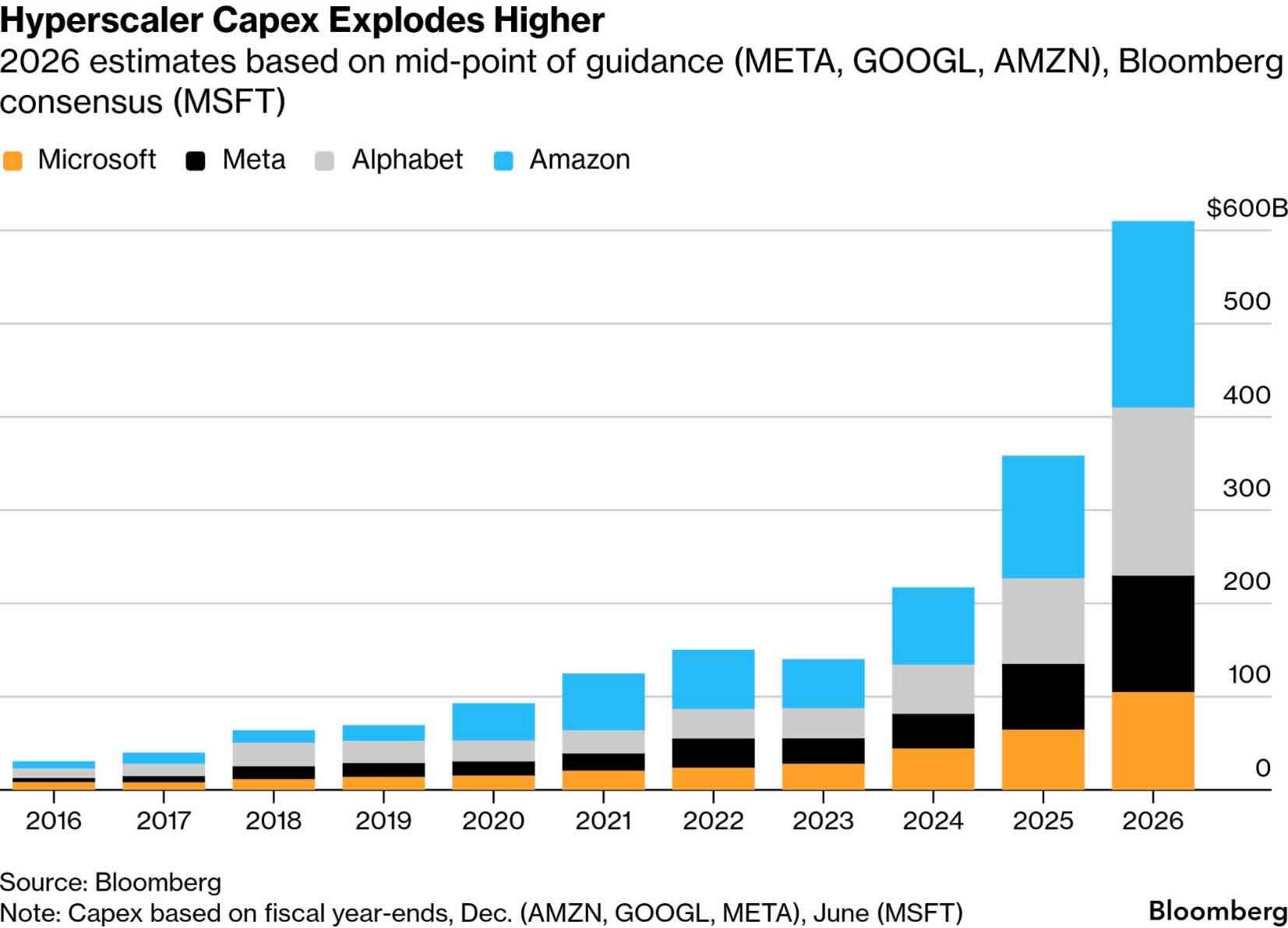

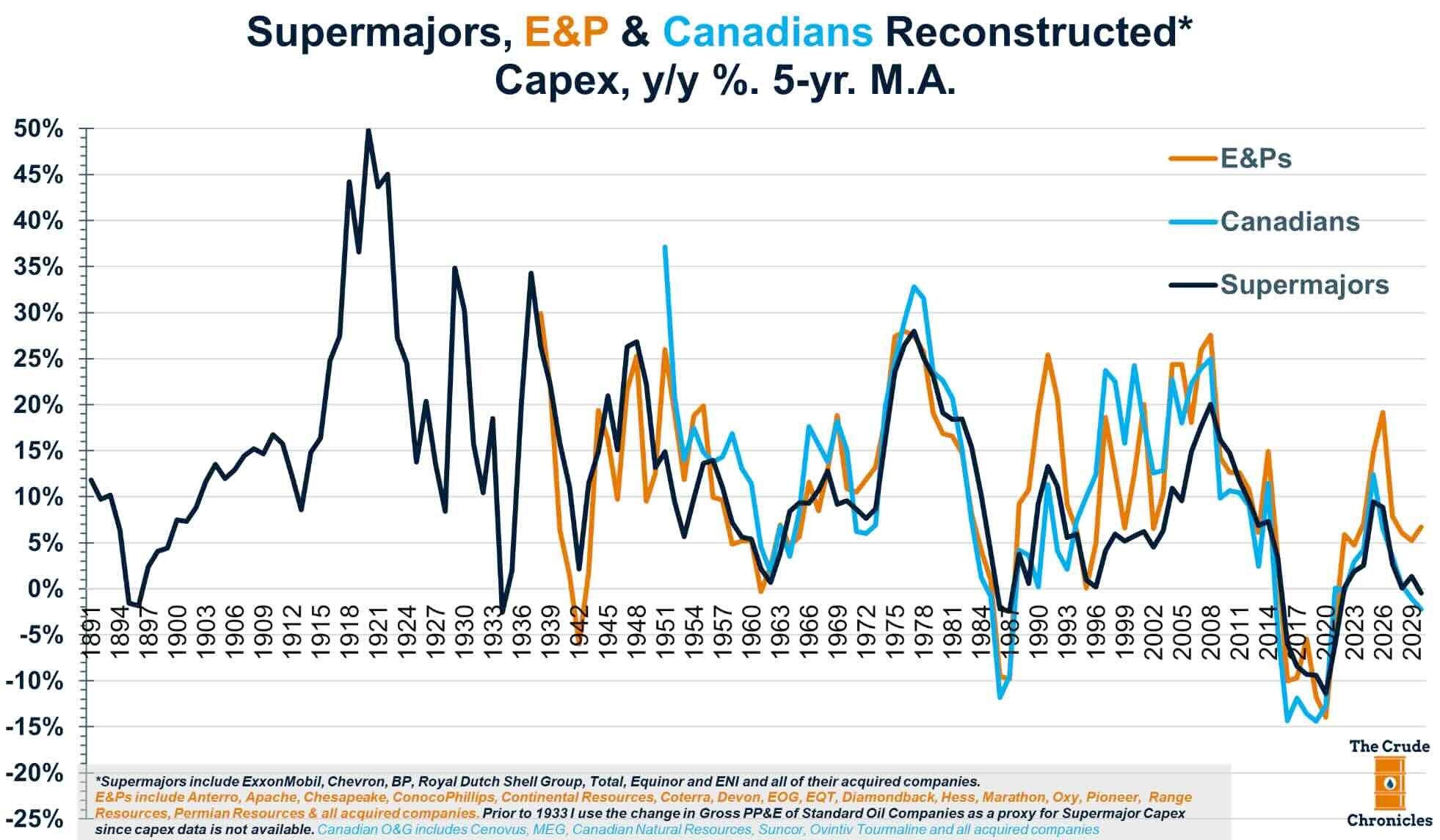

The comparison of tech and energy capex is most blatant… especially since they directly relate to each other.

Capex across tech companies continues to outpace industry projections (as seen from the above 2024 article that underestimated the below chart’s data), which investors seem to embrace.

Meanwhile, the companies that produce energy (especially natural gas) have seen an ever decreasing amount of capex.

I’ll admit that this is a bit of an apples and oranges comparison, because the correlation to oil/gas and tech isn’t 100%.

But I chose to juxtapose these two sectors because they highlight boom and bust cycles perfectly.

The capex being spent by hyperscalers is a classic example of over supply, and vice versa for energy.

This is a directional observation, not a call for a top or bottom.

It’s a simple concept to understand, and the capex imagery in the above charts is easy for anyone to notice.

Keeping It Simple

Everything mentioned above does not suggest that the AI investment trend is overvalued and ready to crash.

It might be, but that’s not what I’m proposing here. (I already made a valuation argument here.)

Instead, I’m pointing out that there are hated sectors of the market that are near the trough of a capex cycle, while there are loved sectors of the market that are near the peak of their capex cycle.

The companies near the tough are trading for earnings multiples in the single digits. Their production capacity is constrained, which will eventually squeeze their product’s prices much higher.

The companies near the peak are trading for high double digit earnings multiples. Their production capacity is rapidly expanding, which will eventually bring more product to market, lowering prices.

Here is the most important part:

A bet on undervalued sectors in the trough of capex investment is not a bet that AI will crash.

It’s simply a bet that the physical world will rerate in order to catch up to the rapidly expanding virtual world.

It’s a when, not if scenario.