Valuation Arbitrage in the AI and Data Center Boom

While the major companies require years of massive growth ahead, others are trading as if the AI boom is already over.

54% of Americans feel like nobody knows them well.

I heard that in church a couple of weeks ago. (Don’t worry, this isn’t a church/religion post.)

That statistic is crazy. Yet, somewhat unsurprising.

Surface level interactions, like the scrolling and consumption of surface level information, seem to be rampant in today’s society.

We’re all looking for the quick hit, the dopamine spike, the immediate gratification.

Few of us are willing to spend the time to get a deeper understanding of anything, or anyone.

Does anyone do deep dives into information, or anyone, anymore?

Or do people just consume headlines and commentary from third parties, never getting to know the depth of what’s really going on?

Can This Narrative Get LOUDER?

I’m pretty good at using AI tools, compared to my peers.

But I have relatively no clue how the tech works.

I understand all of the vocabulary - data centers, tokens, LLM’s, OpenClaw, blah, blah, blah - and I understand the general big picture. I’m even fairly competent at vibe coding.

But I can’t tell you the finer details about why Anthropic is better than Gemini, or why Grok is cooler than OpenAI, or why Amazon’s $200 billion of capex is more strategic than Meta’s $130 billion.

I also can’t tell you how the circle jerk of financing between Nvidia, Oracle, AMD, etc. works.

Maybe it’s all so well thought out and sophisticated that I’m just too stupid to understand it all.

There’s a high possibility of that.

Here’s an example of what I’m talking about:

I understand what this chart is saying. I can even envision a scenario where this data center projection isn’t too outlandish.

The other megaprojects, like railroads and the highway system, were for physically stationed assets within the United States only.

So data centers, which can provide services to anywhere in the world, have a much larger TAM and their possible use cases are a bit broader. The world is also richer, even with inflation adjusted, so we can throw more money at things.

On top of all of that, everyone is saying that you just don’t understand what AI will do to the world.

It will disrupt driving, manufacturing, logistics, mining, communications - it’ll disrupt everything more than you can possibly imagine!

That’s why there’s still so much more room to run with this global AI build out. That’s why the line on that chart will continue to go straight up!

Whether that’s true or not, there’s still something big I don’t understand…

The valuation discrepancies in the companies participating in the AI buildout is wild.

Is it because no one is actually diving into the information, and instead just following the flow of trending narratives?

Valuations With High Expectations

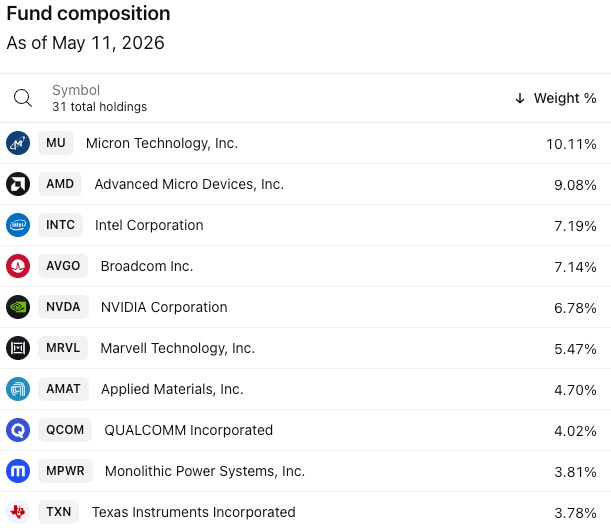

Let’s start with the most obvious components of a data center: semiconductors.

For simplicity, we’ll just look at the SOXX 0.00%↑ Semiconductor ETF, instead of detailing each individual company. Here are the ETF’s holdings:

You can’t argue with the fund’s performance over the past 5 years, which has seen a 300% gain.

But its current valuation makes it one of the highest valued ETF’s on the market.

Trailing P/E: ~50

Forward P/E: ~40

While it’s certainly possible that the ETF constituents could grow into these earnings, it’s also possible that there’s significant downside risk if growth doesn’t keep accelerating.

I’m not going to debate whether or not the valuations of semiconductor companies are over valued or not. There’s plenty of talk out there about that.

Instead, I simply want to juxtapose other companies, which provide important materials for data centers, which are valued drastically lower.

Although most people only think of the costs of semiconductors inside data centers, they actually only make up ~50% of the total cost of the facility.

The rest of the costs go towards electrical power infrastructure, cooling and HVAC systems, construction, cables/fiber, and smaller miscellaneous expenses.

These could be considered the second order beneficiaries of the data center boom. As you’d expect, the top companies in each of those categories have benefitted immensely. Here are just several:

Cooling: Trane Technologies TT 0.00%↑ (P/E = 36)

Electrical: Eaton ETV 0.00%↑ (P/E = 40)

Construction: Emcor Group EME 0.00%↑ (P/E = 30)

Cables/fiber: Corning GLW 0.00%↑ (P/E = 100)

Arguably, the second order company valuations are even more stretched than the semiconductor companies!

With smaller margins, reliance on raw products that have volatile pricing, and one-off projects, it’s hard to see how these companies can maintain their growth.

But, let’s say they do.

Let’s assume that the next decade will see the same growth in data centers around the world. Let’s assume that trillions of dollars continue to flow into this industry.

It will all rely on raw and specialized materials, which are cheap right now…

Valuation Arbitrage

While technologies and companies will certainly change into the future, what they use to produce their products will not.

In the end, we’re all reliant on the atoms that our earth provides.

However these atoms are arranged - either naturally or synthetically - they are all extracted and gathered by companies that are mostly being ignored right now.

That’s surprising when you think about what goes into a data center:

It’s especially surprising when you think about what’s going on in the world right now: energy prices are surging, geopolitical relationships are strained, and traditional flows of global materials are coming to a grinding halt.

Meanwhile the companies that extract and bring those minerals to market are cheap!

Here are seven companies that are integral to the data center build out boom, but have mostly been ignored: