The 65,000% Opportunity - Chinese Food Chain Arbitrage

Food chains in China are unbelievably cheap. Are two bad trends setting up for a huge boom?

Efficiency, consistency, real estate, innovation, and branding - supposedly those are the reasons why the world’s most valued restaurant chain has been successful.

I wouldn’t disagree with those strengths, but there is something else that has led to McDonald’s dominance more than anything else: demographics.

Feeding both baby boomers and their kids, McDonald’s has ridden the demographics wave nearly perfectly.

McDonald’s first flourished in a country with not just a growing population, but a growing consumer population.

During their rapid expansion phase, from 1970-1990, the company’s share price rose by over 65,000%!

Since 1990, MCD 0.00%↑ has “only” returned an annualized 12%.

With over 45,000 locations around the world, McDonald’s will probably dominate for many more years to come. But, when it comes to rapid growth, the burger giant is starting to run out of markets to saturate.

Furthermore, although the company is currently attractively valued compared to the rest of the stock market, there are far better options out there.

That’s especially true when you start to look at Asia, and especially China...

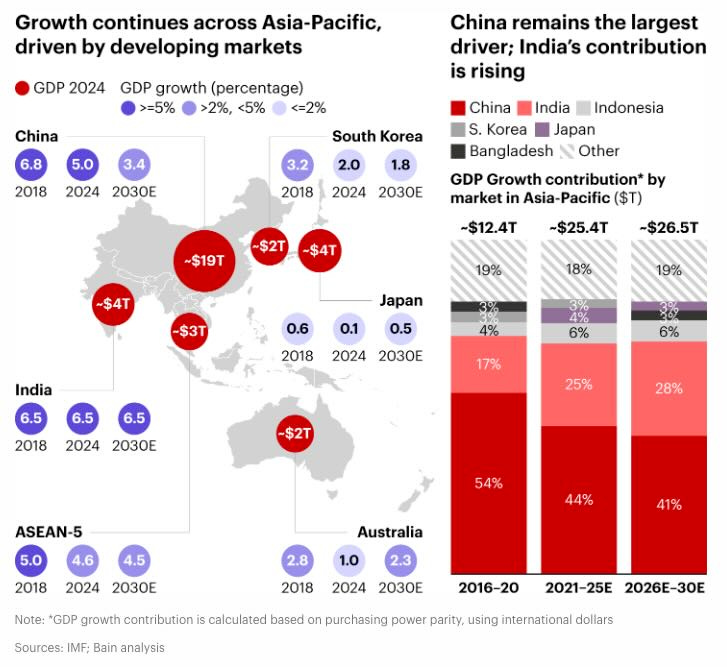

China is Slowing, but Buyers are Growing

Despite all of the doom and gloom, at least from a Westerner’s perspective, there is no doubt that China is still an economic behemoth.

Although China’s GDP growth has slowed down, especially compared to growth rates of regional peers, their total GDP is still massive.

In fact, if you added up all of the Asia-Pacific economies together, they still wouldn’t be as large as China’s.

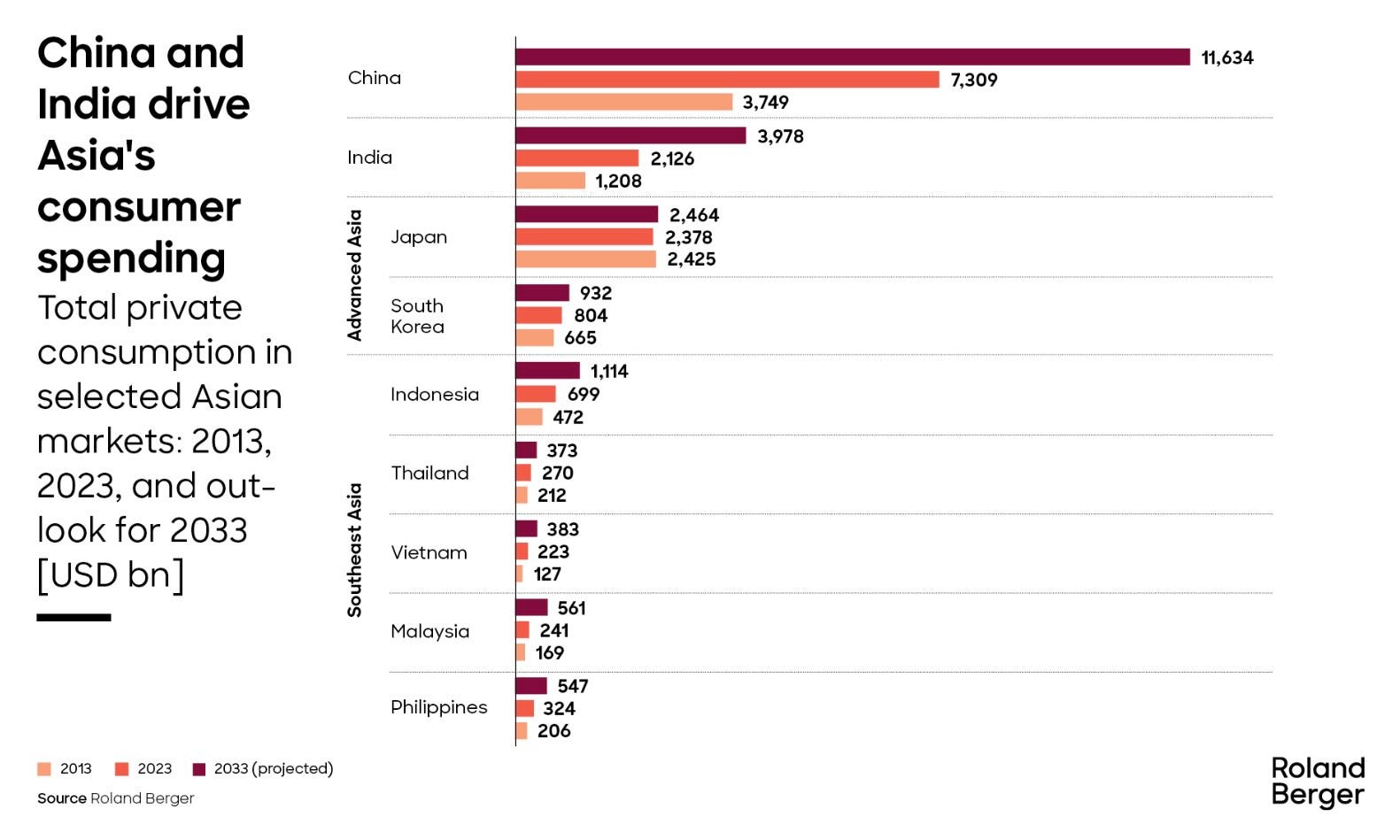

China’s slowing economic growth ignores what that growth is actually achieving: An increase in consumer spending from hundreds of millions of people.

Even with China’s population decline, total private consumption is expected to boom over the coming years.

This story of a rising consumer class is nearly identical to the United States post WWII.

And, as I showed with McDonald’s, some of the companies best situated to benefit from this consumer spending boom are restaurants that exhibit the same qualities of:

Efficiency

Consistency

Real estate

Innovation

Branding

Right now, there are several companies in China that have these exact qualities, yet they are trading for a fraction of their US peers.

And in one case, the same exact brands are trading for a discount - it’s a true arbitrage.

Before we dive into those companies, what has caused this dislocation?

Double Contrarian: China Consumer Cyclical

While one could speculate about weak consumer habits, as seen in the K-shaped economy, there is a more likely culprit: Money is chasing tech and energy due to AI fueled mania and geopolitical chaos.

The companies operating in the consumer cyclical sector appear to have relatively little upside and are simply boring.

In reality, many of these boring companies are seeing impressive, consistently growing earnings.

Then, when we look at China, the weakness within this sector is exacerbated.

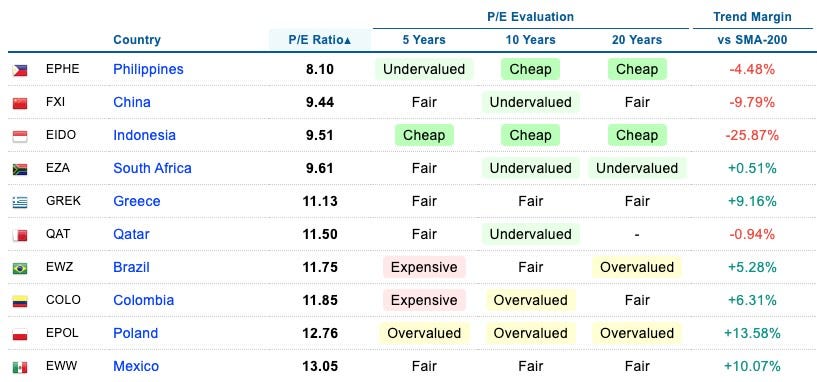

China is certainly slowing down, but it’s still growing. It’s valuation is relatively cheap, and so are the companies that are profitably operating and expanding within the Asian nation.

Now let’s check out three Chinese food companies that are drastically cheaper than their US peers despite arguably better financials.

Each of these companies are virtually debt free with billions in cash just sitting there.

One of the companies has a forward P/E of 6!

A 10x in the coming years is a conservative possibility…

{kind=link}